Articles

2 Things Every Investor Should Know About SECURE Act 2.0

In late December, a $1.7T omnibus spending package was passed in Congress and subsequently signed into law by President Biden. This bill included some significant updates to the landmark 2019 SECURE Act, such that this portion of the legislation is being referred to as SECURE Act 2.0.

While there are many important updates in the law, I’d like to focus on two items that we believe are especially significant

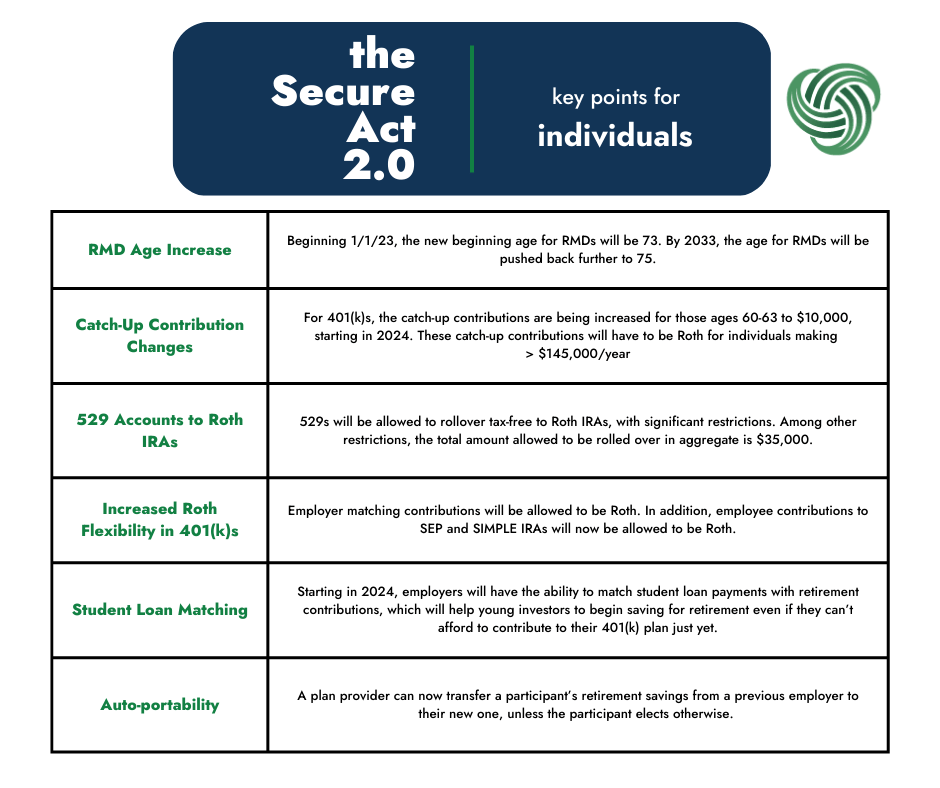

This means that investors who will turn 72 in 2023 received a pass on what would have been their first RMD! It also means that the window of opportunity for income planning in retirement is extended.

Some of the most opportune years in terms of income planning are the years between retirement and when RMDs begin. In these years, individuals tend to be in a relatively low tax bracket, because they no longer have high employment income and they also don’t yet have required income coming from their retirement accounts.

If these retirees are able to live on Social Security and income from taxable brokerage accounts, they could end up in an unusually low tax bracket. These years can then be used to “harvest” capital gains at a 0% tax rate, or convert portions of a traditional IRA to a Roth IRA. The lower adjusted gross income can also help retirees save on things like Medicare and Social Security taxes.

The total amount allowed to be rolled over in aggregate is $35,000, and the rollovers must be done in accordance with the annual Roth contribution limits (currently $6,500 for those under age 50). In addition, the 529 must have been established for at least 15 years.

This change will help to alleviate investor fears of what may happen to 529 funds if the beneficiary chooses not to pursue higher education.

The change also allows for a strategy whereby investors begin planned rollovers to a Roth IRA once the beneficiary turns 16. At today’s limits (which will be adjusted up for inflation), a 529 beneficiary could have $35,000 plus earnings saved in a Roth IRA before graduating from college. That is a solid head start!

If you have questions about how these opportunities could affect your financial planning, please call one of our offices to speak with a wealth manager today.

See below for additional key provisions in SECURE Act 2.0: