Articles

Monthly Market Recap: November 2023

Month in Review

A November to Remember!

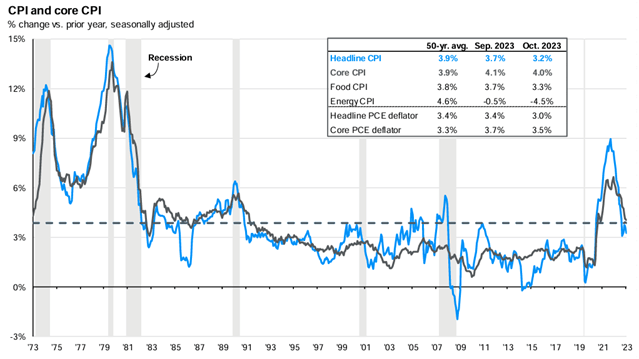

November was a month to remember for investors: The S&P 500 posted its strongest November since 1980 (rising roughly 9%) and the Barclays Aggregate Bond Index had its best month since May 1985 (rising roughly 4.5%).

What were the catalysts for such a sharp reversal?

Investor sentiment had become overly negative – a three-month losing streak for stocks and a 5-month losing streak for bonds. This set-up was followed by unexpected positive developments on the fight against inflation. Multiple readings during November showed inflation rising by less than expectations. Federal Reserve officials also affirmed progress towards normalizing inflation, the decline can be seen in the exhibit below. The positive developments on inflation drove interest rates lower, sending stock and bond prices higher, as investors now shift their attention away from rate hikes to rate cuts.

Source: BLS, FactSet, J.P. Morgan Asset Management. CPI used is CPI-U and values shown are % change vs. one year ago. Core CPI is defined as CPI excluding food and energy prices. The Personal Consumption Expenditure (PCE) deflator employs an evolving chain-weighted basket of consumer expenditures instead of the fixed-weight basket used in CPI calculations. Guide to the Markets – U.S. Data are as of November 30, 2023.

What’s on Deck for December?

Download the November 2023 Market Recap below:

$96 Trillion is going to pass from one generation to the next over the coming 30 years.

This is either going to go smoothly or poorly, and much of that answer will come down to estate planning.

Your estate plan is a crucial aspect of securing your family’s future, and communicating this wealth plan effectively to your children is perhaps even more important.

Here are 4 key strategies to help ensure your heirs are ready:

This might seem basic, but start the conversation early. Don’t wait for a crisis to discuss your estate plan. Start the conversation with your children while everyone is in good health and spirits. Choose a suitable time and place for the discussion, ensuring minimal distractions. This will allow your children to focus on the important matters at hand without feeling rushed or pressured.

Clearly communicate who will be responsible for executing your wishes and managing your affairs if you are unable to do so. If your adult children will be filling these roles, tell them. Don’t assume that your oldest child will understand why you made your middle child the executor. Explain your decisions and choices so that when the time comes there won’t be any confusion or hurt feelings.

You don’t have to share all of the details right away, but make a plan for bringing in the next generation into your financial picture. These discussions are difficult to begin in most households, but at some point you should consider letting your adult children know what you have and how all of it will be transferred. Eventually you should share detailed information about your assets, including properties, investments, and savings. Do you have a financial plan with your financial advisor? It would be wise to share it with your children.

When in doubt, over communicate. You would be amazed at the disagreements that will come up after you are gone, many of which are due to a lack of direction and clarity on your part. Don’t assume your children will know what to do. Spell it out for them.

You don’t have to share all of the details right away, but make a plan for bringing in the next generation into your financial picture. These discussions are difficult to begin in most households, but at some point you should consider letting your adult children know what you have and how all of it will be transferred. Eventually you should share detailed information about your assets, including properties, investments, and savings. Do you have a financial plan with your financial advisor? It would be wise to share it with your children.

When in doubt, over communicate. You would be amazed at the disagreements that will come up after you are gone, many of which are due to a lack of direction and clarity on your part. Don’t assume your children will know what to do. Spell it out for them.

Nobody likes to have these conversations, but they are important. We often talk at Confluence about helping our clients maximize their legacies, and typically children are the most important part of a legacy. We are here to help you facilitate meaningful conversations with the next generation that help you ensure your wealth impacts future generations positively. Don’t wait, the time to communicate is now.

Month in Review

Narrow Market Leadership

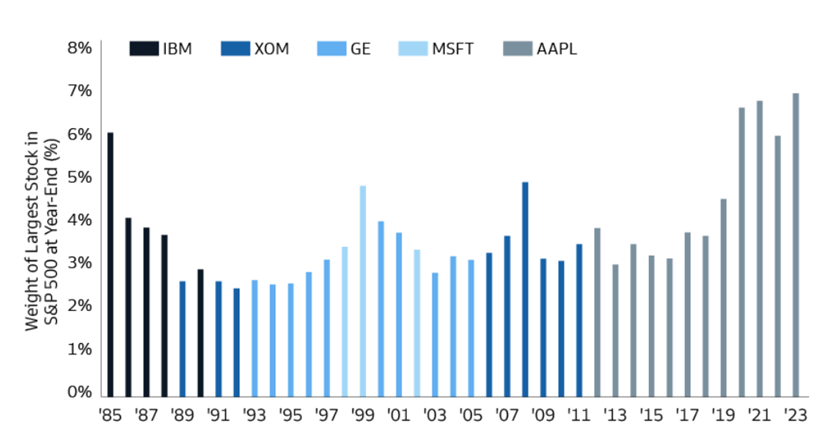

The S&P 500 and growth stocks benefitted from continued strong results from technology companies during 2023. The outsized results of these companies pushed their valuations even higher, with Apple finishing the year as roughly 7% of the S&P 500’s value. This is the largest single weighting in the last 30-years and follows three previous years where Apple represented at least 6% of the S&P 500’s market capitalization. While Apple and six other companies were responsible for the lion’s share of the US stock market’s results in 2023, there are opportunities for broader participation as we head into 2024.

Source: FactSet and Goldman Sachs Asset Management. As of December 31, 2023.

What’s on Deck for January?

Download the December 2023 Market Recap below:

In the past decade, estate tax conversations have been steadily decreasing. As the lifetime credit has climbed to unprecedented highs, many wealthy Americans have come to believe that they are safely out of Uncle Sam’s reach. However, recent history is just that, it’s recent. Historically, estate taxes have been a major factor for both middle class and high-net-worth Americans. Furthermore, estate taxes are often easy targets for adjustments when fiscal gaps need closing. This article explores why estate taxes should continue to be a priority in your wealth planning, and how you can be prepared for whatever the future may hold.

The current estate tax lifetime exemption is $13.61MM per individual, or $27.22MM per couple. These numbers have become so high in recent years, that many high-net-worth Americans have come to believe that they no longer need to worry about estate taxes. My advice is to be careful, because congress can change the rules at any time. As recently as 2008, the exemption was only $2MM per individual, and it was even lower than that in the 1990s and early 2000s. Even under current law if nothing else changes, the $13.61MM exclusion will be cut in half on January 1st of 2026. When tax shortfalls arise, estate taxes are often viewed as low hanging fruit for Washington. The current exclusion level is an aberration, not the historical norm.

The rule of thumb for most families is to have their estate plan documents reviewed every 5 years. However, if you are a high-net-worth individual with an estate tax issue, these reviews should be much more frequent. In fact, estate tax considerations should be a part of your financial plan to be reviewed and discussed at least annually and perhaps more if there is a significant change in the law. Vehicles such as irrevocable trusts and joint insurance policies can help mitigate the risk of owing estate taxes, and these vehicles and strategies should be a part of the normal cadence of planning.

Charitable giving is one of the many strategic ways to avoid estate taxes, especially if you’ve already set aside the amounts that you plan to leave to your children. Wealth that is left to charitable organizations is not subject to the 40% estate tax. This means that instead of giving $600K to your children and $400k to the government, you give $1MM to an organization you care about, or to a foundation or Donor Advised Fund that is run by your children. Most people would prefer that their heirs decide which causes receive those funds rather than a large chunk being sent to Washington.

Your team of professionals should include not only an excellent wealth manager who can help you plan around these issues, but also an attorney and a CPA who are experts in their fields when it comes to estate taxes. These issues are complex, and they can change quickly. Make sure that you are working with professionals who have the knowledge and the bandwidth to give these issues the attention they deserve.

In Summary

Estate planning is a dynamic field that requires regular attention, especially for those with significant wealth. High-net-worth individuals should not only reassess their estate plans frequently but should also consider incorporating charitable giving as part of their strategy. Be sure your planning team includes knowledgeable wealth managers, attorneys, and CPAs as this is crucial as you navigate the ever-changing landscape of estate taxes. Complacency can be costly – proactive estate planning should remain a critical element of your financial health.

If we can be of help to you and your family, please give us a call!

Confluence Financial Partners and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Month in Review

Equity Markets Following Bear Market Recoveries

The S&P 500 reached a new all-time high on January 25th, illustrating the progress the equity market has made following the most recent bear market. Along with making new all-time highs comes an influx of short-term noise, making it important to review the history of market returns following bear market recoveries. Looking at all 14 cases since 1957, the S&P 500 rose an average of 23% over the 18 month period following the 20% recovery from a bear market low. In present day, the S&P 500 had a bear market low on October 12, 2022, and recovered 20% roughly 9 months later in June 2023. Ignoring short-termism around all-time highs, history suggests the equity markets continue to rise after recovering from a bear market.

Source: Yahoo! Finance as of 1/30/2024; BMO Capital Markets via Brian Belski.

What’s on Deck for February?

Whether you are a business owner offering a retirement plan to your employees or are an employee participating in a company sponsored retirement plan, managing the benefit & saving for retirement both can feel like an isolating process. Too often we see a lack of guidance or knowledge from financial advisors to be able to serve as a resource to the company or its employees.

Confluence understands these challenges with a dedicated team of financial advisors collaborating with employee retirement plans. We have built a comprehensive 401(k) service structure – Confluence Standard of Care, designed to offer peace of mind to the employer, while supporting employees to make informed decisions to reach their financial & retirement goals.

Our 401(k) Standard of Care service structure centers on four key pillars:

During these meetings we will discuss the following topics:

2. Employee engagement: Our education team uses highly customized plan participant content structured to help optimize outcomes and increase financial wellness. We deliver multiple types of meetings throughout the year. These meetings run the spectrum from group education to 1on1 individual consultations, and life stage education designed to meet the employee at their individual career stage.

3. Regular investment monitoring & investment analysis: As a member of the Retirement Plan Advisor Group (RPAG), we have access to their proprietary fund ranking system that aims to enhance outcomes, manage risks, and reduce fiduciary exposure. Employers receive quarterly plan “report cards” detailing investments scores. In addition to the fund scores, Confluence has an internal Investment Advisor Committee that provides guidance on selected investment managers and incorporates a qualitative layer of oversight to the fund analysis programs used.

4. Ongoing communication & support: In addition to the processes outlined above, we deliver a variety of additional touchpoints designed to keep employers and participants informed and engaged. This includes informative webinars, quarterly newsletters, and campaigns to address specific plan demographics or concerns.

By utilizing these services, employers can have the confidence in knowing their 401(k) is managed effectively while employees have the opportunity to understand their benefits options.

Our team is here to guide you every step of the way. Should you have any questions or require further information on how our service delivery model can benefit your organization, please do not hesitate to contact us or listen to our podcasts today!

Confluence Wealth Services, Inc. d/b/a Confluence Financial Partners is a SEC-registered investment adviser. Confluence Financial Partners only transacts business in states where it is properly registered or notice filed or excluded or exempted from registration requirements. The security of electronic mail sent through the Internet is not guaranteed. All email sent to or from this address will be received or otherwise recorded by the Confluence Financial Partners corporate email system and is subject to archival, monitoring and/or review, by and/or disclosure to, someone other than the recipient. Confluence Financial Partners recommends you do not send confidential information to us via electronic mail, including social security numbers, account numbers, and personal identification numbers, unless properly encrypted. A copy of our current written disclosure statement discussing our advisory services and fees continues to remain available for your review upon request or by visiting the following link:https://www.confluencefp.com/form-adv-2a/

Month in Review

Attention to Interest Rates

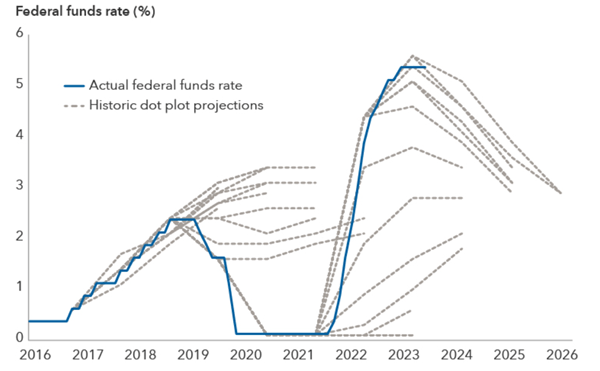

Investors are curious as to when the Federal Reserve will start lowering interest rates. During February, investors recalibrated expectations once again for the start of rate cuts, believing that the first reduction will be pushed back to June 2024. This change makes sense for various reasons: inflation continues to remain somewhat firm, and the labor market remains very strong.

Historically, forecasting the path of interest rates has been notoriously difficult to do and ultimately, introduces unwarranted noise into investors’ outlooks. The chart below shows how even the Federal Reserve struggles to predict its own interest rate decisions.

Source: Capital Group, Bloomberg. As of February 23, 2024. Federal funds rate data from January 2016 to February 2024. Forward looking dot plot projections are reported quarterly from September 2016 through December 2023.

What’s on Deck for March?

What is your time ratio? Here are a few thoughts to consider:

10% – Past

We benefit greatly from history, experiences, and lessons from our past. Unfortunately/fortunately, the past is over. We can no longer control or change it. Hold on to the positive experiences and valuable lessons, and leave the regrets behind.

60% – Present

It’s really all we have! Living in the moment is a gift. Waking up to the now and having a “be where your feet are” attitude is an important perspective to keep as you focus on the present. Let’s be careful not to allow fear, or distractions like cell phones, to steal our moments.

30% – Future

Happiness comes from believing your best days are ahead. Planning reduces stress, creates energy and increases the likelihood of a bright future. Don’t wonder if your best days are ahead of you, take concrete steps so that you can be sure!

Let’s encourage each other to learn from the past, live in the present and believe in the future.

We are grateful to be a part of your journey!

Month in Review

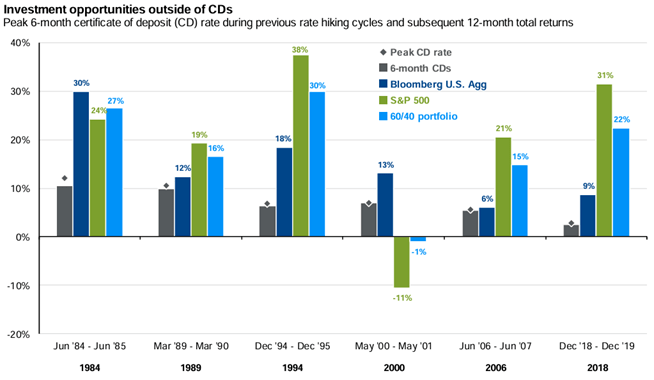

Time to Look Beyond Cash?

Last month we discussed the difficulty in forecasting changes in interest rates. During March, investors spent the month aligning their outlook with the Federal Reserve’s guidance, which remains some level of interest rate cuts sometime later this year. While the exact timing cannot be known, we do know that historically there have been opportunities to shift out of cash investments near peak interest rates.

Going back to the six previous cycles since 1984, investors have been better off investing in bonds, US stocks or a balanced portfolio compared to staying in cash during the 12-months following the peak level of interest rates. Forecasting the exact time of peak interest rates/rate cuts is fruitless, but for long-term investors there is an opportunity to look beyond cash.

Source: Bloomberg, FactSet, Federal Reserve, Robert Shiller, J.P. Morgan Asset Management. The 60/40 portfolio is 60% invested in S&P 500 Total Return Index and 40% invested in Bloomberg U.S. Aggregate Total Return Index. The S&P 500 total return figure from the 1984 period was calculated using data from Robert Shiller. The analysis references the month in which the month-end 6-month CD rate peaked during previous rate hiking cycles. CD rate data prior to 2013 are sourced from the Federal Reserve, whereas data from 2013 to 2023 are sourced from Bloomberg. CD subsequent 12-month return calculation assumes reinvestment at the prevailing 6-month rate when the initial CD matures.

What’s on Deck for April?

Our mission at Confluence Financial Partners is to Maximize Lives and Legacies.

As our industry has evolved, we understand that the role of a wealth management firm has become bigger than simply managing portfolios and building financial plans. While plans and portfolios remain essential, we believe that true wealth lies not only in financial abundance but also in physical and mental well-being. Studies show that individuals who prioritize their health tend to experience enhanced cognitive function, increased productivity, and overall improved quality of life.

In light of this, it is with much enthusiasm that we announce the addition of a dietitian to our team at Confluence, Sarah Rupp, MS, RD, LDN!

Our commitment to associates and clients is to expand beyond the conventional boundaries of wealth management and we believe the addition of Sarah helps us deliver that commitment.

We look forward to sharing Sarah’s knowledge to further Maximize Lives and Legacies.

Great Days Ahead!

Greg Weimer, CEO