Insights

Market Pulse: Quarter 1, 2025

The first quarter of 2025 has been a period of dynamic shifts in global financial markets, marked by evolving economic policies, heightened uncertainty, and increased volatility equity markets. In this edition of Market Pulse, we analyze key investment trends, including the broad rotation from growth to value stocks, the resurgence of international equities, and the stabilizing role of fixed income markets.

Despite market volatility, history reminds us that corrections are a natural and expected part of long-term investing. The recent pullback in the S&P 500, while significant, aligns with historical trends, reinforcing the importance of diversification and disciplined investment strategies. International markets, buoyed by fiscal stimulus measures, have provided investors with new opportunities, while fixed income markets have continued their recovery.

Looking ahead to the second quarter, trade and fiscal policy developments will remain critical factors shaping investor sentiment. By maintaining a strategic and diversified approach focused on their objectives, investors can navigate uncertainty and capitalize on emerging opportunities. On behalf of Confluence Financial Partners, we thank you for your continued trust and confidence.

Bill Winkeler, CFA, CFP®

Chief Investment Officer

Diversification Renaissance

• Uncertainty around the implementation of new policies and softening economic data weighed on markets

• S&P 500 had its worst quarter since 2022 and its first correction (> 10% decline) since October 2023, an event that historically happens roughly 1.5 years

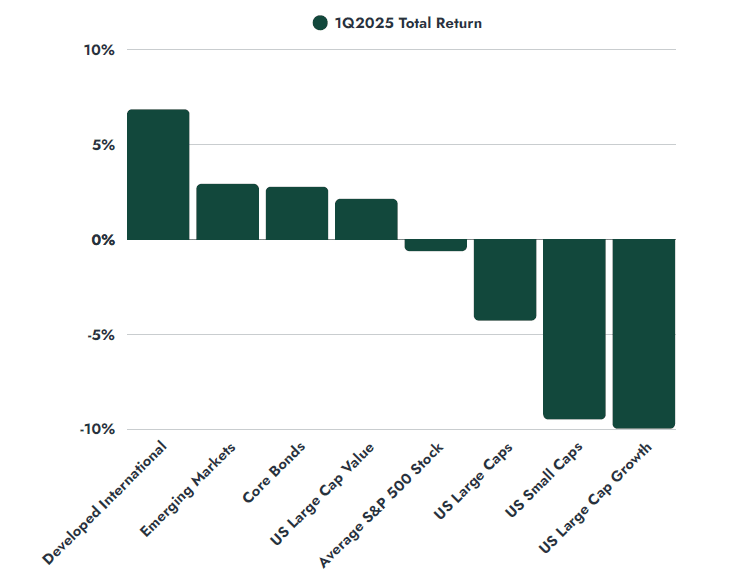

• This sparked a rotation away from Magnificent 7 and Technology stocks to Value and International stocks, with international stocks posting their best relative quarter in over 25 years

What Happened in the First Quarter?

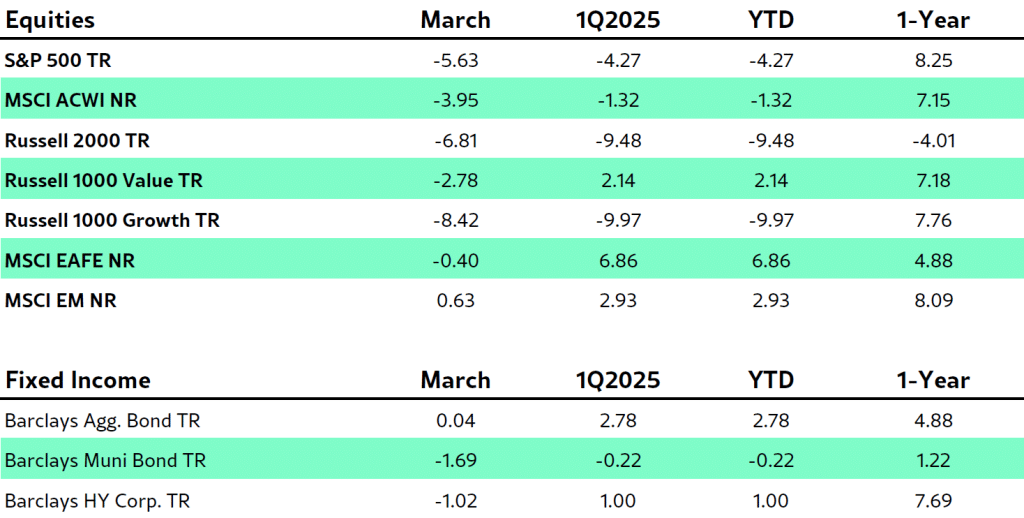

Investors spent the first three months of 2025 digesting the implementation of new policies, along with a shifting outlook for the economy. While “uncertainty” is often over-used, measures of uncertainty around trade and outlook for the economy spiked to very high levels, as investors sought more clarity around tariffs and related trade policies. The increase in uncertainty, combined with some softening of economic data (for example a mild increase in unemployment), helped to drive the first correction (decline greater than -10%) in the S&P 500 since October 2023. Previous market leaders – the “Magnificent 7” growth companies in the S&P 500 Index, were hit harder than the rest of the market, falling roughly -15% during the quarter. Importantly for investors, other equity markets and fixed income markets provided diversification benefits in the first quarter, and S&P 500 earnings expectations for 2025 have remained largely stable.

Diversification Means “You’re Always Having to Say You’re Sorry”

The old adage for diversified investors was invoked frequently in 2023 and 2024, in an equity market led by a handful of US large growth companies. Early in 2025, diversified investors have had the chance to say “thank you”, as investors have rotated away from US large cap growth companies, into large cap value stocks, international stocks and bonds. Even within the S&P 500 Index, the Magnificent 7 Stocks fell roughly -15%, while the remaining 493 stocks in the S&P 500 Index were flat for the quarter.

Sources: Morningstar, Average S&P 500 Stock = S&P 500 Equal Weighted TR Index, US Large Caps = S&P 500 TR Index, US Large Cap Value = Russell 1000 Value TR Index, US Large Cap Growth = Russell 1000 Growth TR Index, US Small Cap = Russell 2000 TR Index, Developed International = MSCI EAFE NR Index, Emerging Markets = MSCI Emerging Markets NR Index, Core Bonds = Bloomberg US Agg Bond TR Index

The start to 2025 for international stocks has been one of the strongest in the past 25 years, as US investors benefitted from both rising foreign stock prices and the depreciation of the US dollar. International equities have been inexpensive but lacking strong fundamental catalysts, which began to change during the quarter. In Europe, Germany introduced a very large fiscal spending package to stimulate their economy, the largest in their history (exceeds the Marshall Plan and Reunification). The changing attitudes towards spending by European countries has been well received by investors.

Results for fixed income investors continued the positive trend in the first quarter of 2025 as well. After the worst calendar year in its history in 2022 (-13.01%, Bloomberg US Aggregate Bond TR index, data back to 1926), the bond index posted a gain of +2.78% in 1Q2025. This follows consecutive calendar year gains in 2023 (+5.53%) and 2024 (+1.25%). Interest rates have declined across the yield curve, with the 10-year Treasury yield finishing the quarter at 4.23%, down from intra-quarter highs of 4.79%.

Very Average Correction

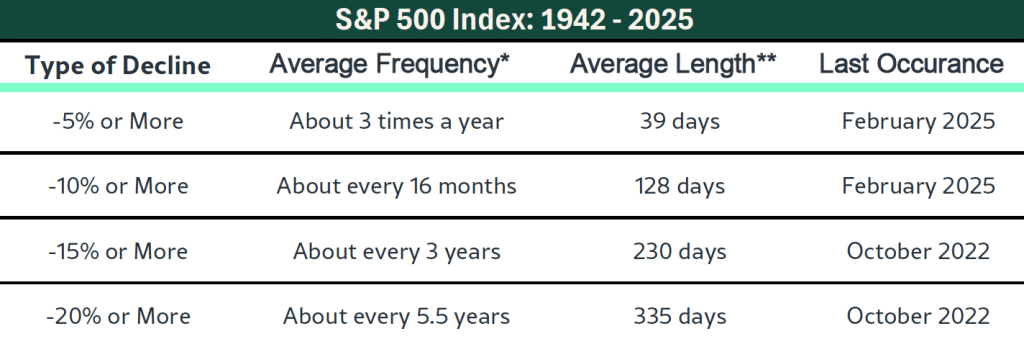

In the previous edition, we noted that 2023 and 2024 were very strong years for the US equity market “The strong year for the S&P 500: 57 new all-time highs and consecutive +25% calendar year gains, was thanks in very large part to the largest companies in the index.” Early in 2025, investors were reminded that volatility is a very normal and common feature of equity market investing. From February 19th, the S&P 500 fell over -10% in less than 30 days, making it the 11th fastest correction since 1928. Quickness aside, the frequency was very average – 60th correction since 1926, the first since October 2023, right on the historical average frequency. Investors may be wondering if this will turn into a bear market (a decline greater than -20%): while no one has a crystal ball, out of the 59 previous corrections since 1926, only 17 ended up turning into a bear market (roughly 29%). The S&P 500 recently experienced a bear market in October 2022.

Source: First Trust, Bloomberg. Data from 4/29/1942 – 2/28/2025. Past performance is no guarantee of future results. For illustrative purposes only and not indicative of any actual investment. Investors cannot invest directly in an index.*Correction cycles are determined by identifying market declines in excess of the minimum declines noted above. The cycle ends when there is a recovery of the magnitude of the minimum decline needed for that correction size (i.e., a recovery of greater than 5%, 10%, 15% or 20%). After that recovery is noted, the algorithm begins searching for the next decline to start the cycle again. **Measures from the date of the market high to the date of the market low. The S&P 500 Index is an unmanaged index of 500 companies used to measure large-cap U.S. stock market performance.

Corrections and bear markets, along with normal intra-year declines, are the toll investors pay for the long-term results of equities. Since 1980, the S&P 500 TR Index has had average annual declines of roughly 14% every year but still finished the calendar year in positive territory 75% of the time. This illustrates the importance of staying invested during volatility and ensuring that your investment portfolio is aligned with your objectives and financial plan.

What’s Ahead for the Second Quarter?

Changes to trade policy are having a tangible effect on investor and consumer sentiment, with the potential to negatively impact economic growth. Both investors and the Federal Reserve are looking for greater clarity on how additional tariffs could be implemented, which will play a key role in any changes to the Federal Funds Rate in 2025. Within fiscal policy, any changes to tax policy in the United States are trending towards happening later in 2025, but developments there will be watched closely by investors. As discussed, international equities have benefitted from a strong fiscal impulse from Europe, with the implementation likely to be in focus during 2Q2025.

Markets In Review

For many business owners, their company represents more than just a source of income—it is a legacy built through years of dedication and perseverance. Ensuring the continuity of that legacy requires careful, strategic planning. Business succession planning is the structured process of transitioning ownership and leadership, helping to secure long-term stability and success for future generations.

However, succession planning is not merely about selecting a successor. It involves developing a comprehensive strategy that mitigates risks, maximizes business value, and lays out a seamless transition path. Without a well-defined plan, companies may face uncertainty, internal conflict, or disruptions that could negatively impact operations. A thoughtfully executed succession plan can help business owners to retire with confidence, knowing their company is in capable hands.

Establishing a Business with Long-Term Vision

One of the most important decisions a business owner can make is whether they are building their company for longevity or positioning it for sale. This fundamental choice can influence leadership development, financial planning, and operational strategy.

When a business is designed solely with an eventual sale in mind, decision-making tends to prioritize short-term gains over long-term stability. Cost-cutting may take precedence over investing in innovation, employee growth, and customer relationships. While this may enhance financial performance in the short term, it can leave the business fragile and ill-prepared for a smooth transition of ownership.

Conversely, a company built with the future in mind can be better positioned to withstand the challenges of leadership transitions. Owners who focus on long-term success tend to make strategic investments in their workforce, establish strong corporate values, and implement scalable systems that help ensure adaptability in a changing market. These efforts can not only help strengthen the business but also can enhance its appeal to potential successors, whether they are internal leaders or external buyers. Ultimately, businesses with a legacy-driven approach are better positioned to thrive across generations.

Key Components of a Successful Business Exit Strategy

Ultimately, a business owner will likely want to exit the business through a well-thought out plan. If the business is going to survive into the future, the business exit strategy should carefully examine all aspects of the transition. Here are a few key components:

The Role of a Wealth Management Firm in Business Succession Planning

Navigating the complexities of business succession planning often requires professional guidance. Partnering with a wealth management firm like Confluence Financial Partners can be invaluable in creating a smooth transition. Our team of financial professionals can assist with various aspects of the process, including:

Securing Your Legacy for Future Generations

Business succession planning is not a task to be postponed. Proactively creating a structured exit strategy can help enable a seamless transition, safeguard your company’s legacy, and provide financial security for both you and your successors. Working with a trusted wealth management firm can also simplify the process and help ensure that your business remains strong for generations to come.

If you are considering business succession planning, we encourage you to take the first step. Contact Confluence Financial Partners today to discuss crafting a customized succession planning strategy tailored to your unique business needs.

Investing can be a powerful tool for building wealth and helping to secure financial stability, but to maximize its benefits, it should be aligned with your personal financial goals. A Financial Plan, supported by the professional guidance of a Wealth Management firm, such as Confluence Financial Partners, can help your portfolio reflect your long-term aspirations. Here are a few key steps to help make sure your financial plan drives your investing decisions.

1. Define Your Financial Goals

Before diving into investing or reassessing your current investments, it is best to establish clear financial objectives. Are you investing for retirement, a major purchase, or perhaps even leaving a legacy for your children? Whatever your objectives are, you should evaluate your existing investments to ensure they still align. A Certified Financial Planner (CFP) or Financial Advisor can help you set realistic, time-bound goals that serve as a foundation for your investment strategy.

2. Develop a Financial Plan

A well-crafted financial plan can serve as the foundation of a successful investment strategy. It starts with a clear understanding of your financial goals, risk tolerance, and time horizon. A comprehensive plan should incorporate key elements such as budgeting, debt management, savings, and insurance to establish a strong financial footing. It should also define both short-term and long-term objectives, providing a structured roadmap for building and preserving wealth. By thoroughly evaluating your current financial situation and anticipating future needs, a strategic plan can empower you to make informed investment decisions that support your overall financial well-being.

Confluence Financial Partners takes a holistic approach to financial planning and can help provide you with actionable steps to integrate the aspects of your financial life seamlessly. Rather than viewing investments in isolation, Confluence works to align them with cash flow management, tax strategies, estate planning, and risk mitigation to create a cohesive and strategic path toward your goals. This coordinated approach can help maximize wealth accumulation and long-term financial security, give you clarity and confidence in your decisions. With a well-defined plan in place, you can move forward with greater confidence that your financial future is built on a solid, strategic foundation.

3. Optimize for Tax Efficiency

An essential component of financial planning is optimizing for tax efficiency. Tax considerations can significantly impact investment returns, and working with a Certified Financial Planner (CFP) or Financial Advisor can help minimize tax burdens through strategies such as tax-loss harvesting, asset location planning, and retirement account maximization. By integrating these tax-efficient approaches, after-tax returns could increase and more of your wealth can be put to work toward your financial future.

4. Review, Monitor, and Adjust Your Investments Regularly

Beyond initial planning, continuous review and monitoring of investments can be critical to long-term success. As your life and goals change, your investment strategies should also adapt. Regularly assessing your portfolio in light of your plan can help it remain aligned with your financial objectives. Whether you’re starting fresh or reevaluating existing investments, partnering with a wealth management firm can provide professional oversight, helping to navigate market fluctuations and build a portfolio to help you live the life you want to live. With a proactive approach and professional guidance, you can more confidently pursue financial security and long-term prosperity.

5. Work with a Wealth Management Firm

Confluence Financial Partners is committed to a disciplined approach, guided by five key principles, to shape effective investing strategies. We manage investments to achieve individual client goals, not to beat arbitrary benchmarks. Our objective approach combines active and passive strategies, strategic planning, and tax-efficient solutions to help maximize returns and minimize long-term costs.

The Five Principles of Investing at Confluence Financial Partners

Confluence Financial Partners offers professional guidance in investment planning, risk management, and long-term financial strategy, providing clients with confidence and clarity in their financial journey. By leveraging the knowledge of experienced professionals, we can help develop a structured approach to investing that aligns with your financial aspirations and adapts to changing economic landscapes.

Final Thoughts

Investing is more than just buying securities—it’s about strategically growing your wealth in alignment with your personal financial goals. It’s about helping make sure that you aren’t just saving for saving’s sake, but rather you are building wealth while maximizing both your life and legacy. With the guidance of a Certified Financial Planner (CFP) or Financial Advisor, you will have someone to assist you with your investment decision as you work towards the life that you want. Working with Confluence Financial Partners provides access to our dedicated team that offers strategic insight, thoughtful guidance, and tailored solutions which can help turn your financial aspirations into reality.

Month in Review

Broadening Participation in the Bull Market

With two months in the books, early in 2025 investors have seen signs of broadening participation in the bull market that started in October 2022. From an asset class lens, developed international stocks (MSCI EAFE NR Index) are off to a strong start this year, rising +7.30%, compared to +1.44% for the S&P 500 TR Index. Value stocks are also leading growth stocks in 2025, with the Russell 1000 Value TR Index rising +5.05% versus large cap growth (Russell 1000 Growth TR Index) falling -1.69%.

Early in the year, investors can also see a shift within the S&P 500 Index itself. After being responsible for over 50% of the calendar year returns in 2024, 2023, and 2022, the so-called “Magnificent 7” stocks are trailing the rest of the index. In 2025, the S&P 500 excluding the Magnificent 7 stocks is up +3.2% YTD, and the average stock in the index is up +2.87% (S&P 500 Equal Weight TR Index), ahead of the overall index. One reason for this shift is the trade-off between the high valuations of the Magnificent 7 and the leveling-off of their earnings growth.

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. The top 10 S&P 500 companies are based on the 10 largest index constituents at the beginning of each quarter. As of 2/28/2025, the top 10 companies in the index were AAPL (7.2%), NVDA (6.1%), MSFT (5.9%), AMZN (3.9%), GOOGL/GOOG (3.6%), META (2.9%), BRK.B (1.9%), AVGO (1.8%), TSLA (1.6%), and JPM (1.5%). The remaining stocks represent the rest of the 492 companies in the S&P 500.

The largest companies in the S&P 500 are still expensive relative to their history at 27.3x forward earnings, even after seeing their valuations fall in 2025. Investors have started the year favoring opportunities with cheaper valuations, a trend that has helped diversified investors.

What’s on Deck for January?

When it comes to financial planning and investment management, selecting the right advisor is one of the most critical decisions you can make. One term you may frequently encounter is “RIA,” which stands for Registered Investment Advisor. But what does that really mean, and why is it important for those seeking professional financial guidance?

Understanding an RIA

An RIA is a firm or individual registered with the Securities and Exchange Commission (SEC) or a state regulatory agency, depending on the assets under management. RIAs provide financial advice and investment management services while adhering to strict regulatory requirements designed to protect investors.

At Confluence Financial Partners, being a Registered Investment Advisory means that we are committed to transparency, personalized service, and, most importantly, acting in our clients’ best interests.

The Fiduciary Standard: Acting in Your Best Interest

One of the most significant distinctions of an RIA is the fiduciary duty it upholds. As fiduciaries, RIAs are legally and ethically required to prioritize their clients’ financial well-being above all else. This obligation includes:

At Confluence, our fiduciary responsibility guides financial strategies and tailors them to your unique situation, helping you pursue goals with confidence.

What to Expect When Working with a Registered Investment Advisor

Choosing to work with a Registered Investment Advisor like Confluence Financial Partners provides several opportunities:

What This Means for Confluence Clients

For clients of Confluence Financial Partners, our status as a Registered Investment Advisor represents a commitment: our commitment to act with integrity, to provide prudent guidance, and to help you achieve financial confidence. We embrace our fiduciary duty because we believe that trust is the foundation of every successful financial relationship. Whether you’re planning for retirement, growing your wealth, or navigating complex financial decisions, you deserve an advisor who is not only experienced but also required to put your best interests first.

Take the Next Step with an RIA You Can Trust

If you’re looking for a financial partner who prioritizes your goals and well-being, we invite you to start a conversation with Confluence Financial Partners. Let’s work together to build a strategy that aligns with your vision for the future.

Month in Review

Stocks are Rarely Average

Last year marked the second consecutive year the S&P 500 returned over 25%, making it only the fifth time since 1926 that the index has produced consecutive results of that magnitude. While there have been positive developments in 2025, the fact still remains that the S&P 500 is very concentrated in the top 10 companies, which have pushed the S&P 500’s valuation to above-average levels. How should investors think about this data?

History is a great starting point, with over 100 years of various market conditions, recessions, and geopolitical headlines. History shows that stocks typically have “better-than-average” and “great” years in clusters, much like the S&P 500 has experienced recently. Since 1926, the S&P 500 has averaged 10.4% per year; during that period, it has only posted calendar year returns around the average (8% to 12%) in 6 years. This shows that over longer periods, fundamentals drive stock prices, not year-to-year price fluctuations- the benefit of being a long-term investor.

In addition to understanding historical trends, investors should recognize the broadening out in the current bull market. In January, the S&P 500’s Technology sector was the only sector to fall during the month; the average stock also finished ahead of the index. Investors should view developments such as these favorably as the current bull market continues ahead.

Source: Morningstar as of 12/31/24. U.S. stocks are represented by the S&P 500 Index from 3/4/57 to 12/31/24 and the IA SBBI U.S. Lrg Stock Tr USD Index from 1/1/26 to 3/4/57, unmanaged indexes that are generally considered representative of the U.S. stock market during each given time period.

What’s on Deck for February?

We are excited to share the inaugural version of Confluence Financial Partner’s Market Pulse: A Quarterly Review of Investment Trends and Insights. We aim to succinctly recap key investment trends and events on a quarterly basis, while providing insightful and actionable outlooks for the coming months.

Q4 2024 Insights: Three Key Takeaways

Policy Shift: 2024 saw the Federal Reserve shift gears and lower interest rates, ending the rate hiking cycle that began in June 2022 and featured 9 rate hikes.

Mega Leadership: Mega cap stocks, the largest companies in the US, pulled the S&P 500 to a second consecutive +25% annual gain, outpacing smaller stocks, international stocks, and bonds.

High Concentration: The mega cap leadership resulted in a very narrow market by historical standards: the top 10 stocks in the S&P 500 represent over 38% of the index (highest in over 40 years).

As we enter the new year, don’t wait to implement tax strategies that could improve your financial situation. For investors, smart tax strategies can mean keeping more of what you earn and maximizing the value of your portfolio. Here are some key approaches to consider as you plan for 2025:

1. Maximize Tax-Advantaged Accounts*

Contributing to tax-advantaged accounts like 401(k)s, IRAs, and Health Savings Accounts (HSAs) can reduce your taxable income. For 2025, the 401(k) contribution limit is $23,500 for those under 50, with an additional $7,500 catch-up contribution for those 50 and older. A new provision allows individuals aged 60 to 63 to make an enhanced catch-up contribution of $3,750 in addition to the traditional catch-up contribution, providing a significant opportunity to boost retirement savings during those critical pre-retirement years.

Traditional IRAs also allow for tax-deferred growth, and contributions may be deductible depending on your income and retirement plan coverage.

Roth accounts, while funded with after-tax dollars, offer tax-free withdrawals in retirement—a great option if you expect to be in a higher tax bracket later.

2. Utilize Qualified Charitable Distributions (QCDs)**

If you’re 70½ or older, a Qualified Charitable Distribution (QCD) allows you to donate up to $108,000 directly from your IRA to a qualified charity. This strategy not only satisfies your Required Minimum Distribution (RMD) but also reduces your taxable income. By directing funds straight to the charity, you avoid having the distribution counted as part of your Adjusted Gross Income (AGI), which can help minimize taxes on Social Security benefits or Medicare premiums. This approach is particularly advantageous for retirees who wish to support charitable causes while managing their tax liabilities efficiently.

3. Gift Appreciated Securities

Instead of donating cash or selling investments to give proceeds, consider gifting appreciated stocks or mutual fund shares directly to family members or charities. By gifting to family members in lower tax brackets, they may pay significantly lower taxes on the capital gains, or possibly none at all, depending on their income level. For charitable donations, you can deduct the fair market value of the securities while avoiding the capital gains tax you’d incur if you sold them. This dual benefit maximizes the impact of your gift while offering meaningful tax savings. It’s a smart way to reduce the tax burden on highly appreciated assets.

4. Be Strategic with Municipal Bonds

Municipal bonds, often referred to as “munis,” offer a reliable source of tax-free interest income at the federal level. If you purchase bonds issued by your home state, you may also avoid state and local taxes. For high-income earners, the tax-equivalent yield of municipal bonds can be more attractive than taxable bonds, especially if you’re in the highest federal income tax brackets. Additionally, municipal bonds are generally considered lower-risk investments, providing steady income without increasing your taxable income—a win-win for those seeking both stability and tax efficiency. Whether you should own taxable or tax-free bonds, however, is unique to each individual and should be analyzed as such.

5. Stay Informed on Tax Law Changes*

Tax laws are dynamic, and staying informed helps ensures you’re prepared to adapt your strategy to new opportunities or avoid pitfalls. The individual tax cuts introduced under the 2017 Tax Cuts and Jobs Act (TCJA) are set to expire at the end of 2025 unless new legislation extends them. This includes potential increases in individual income tax rates, a reduction in the standard deduction, and a lower threshold for estate tax exemptions, which may revert to pre-2018 levels—around $7 million per individual instead of the current $14 million. By monitoring legislation, you can adjust your portfolio and tax strategies proactively.

Take Action Now

The key to effective tax planning is proactive management. By leveraging these strategies, you may be able to reduce your tax bill and keep more of your income in 2025. Don’t wait until the end of the year to start planning! Schedule a consultation with one of our experienced wealth managers today to discuss personalized strategies that align with your financial goals.

Sources:

*https://www.morningstar.com/personal-finance/your-tax-fact-sheet-calendar

Confluence Financial Partners does not provide tax advice. You should consult your own tax advisors before engaging in any transaction.

When it comes to estate planning, your beneficiary designations are one of the most critical yet often overlooked components. These designations determine how your assets—such as retirement accounts, life insurance policies, and annuities—are distributed upon your passing. Beneficiary designations often supersede other estate documents, making it essential to ensure they are accurate and up to date.

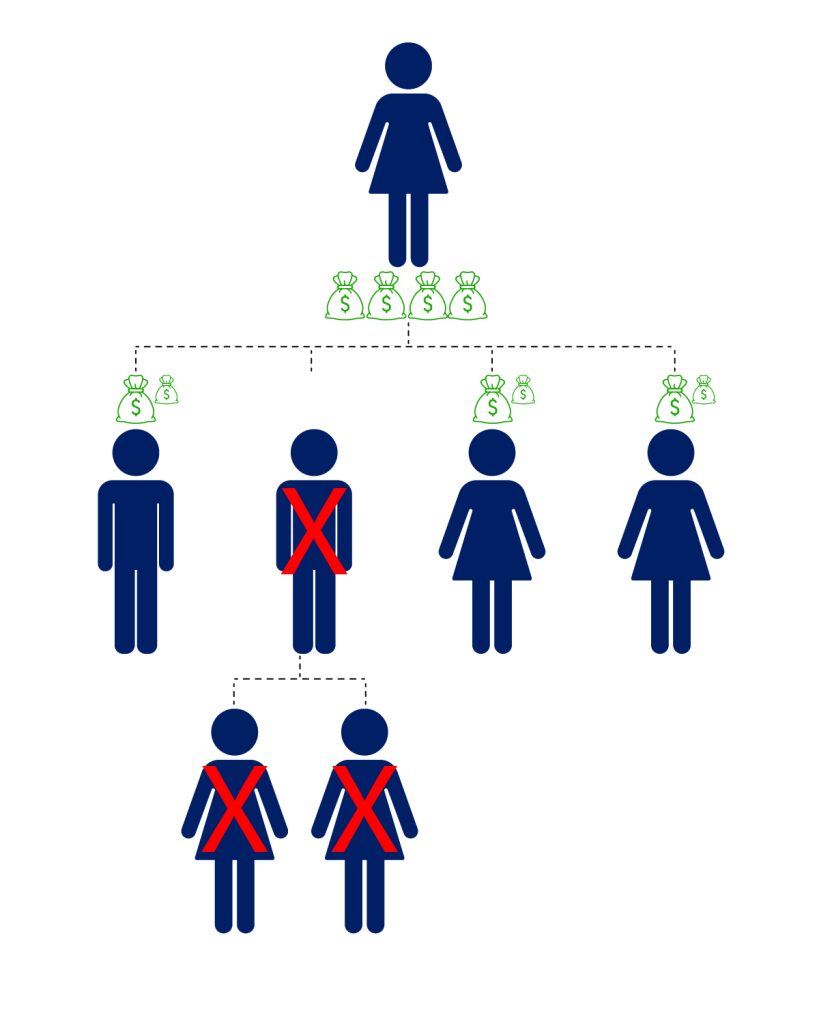

Understanding the Key Difference: Per Capita vs. Per Stirpes

When naming individual beneficiaries, two terms that frequently come up in this context are “per stirpes” and “per capita”. While these terms may seem similar, they represent very different ways of dividing an inheritance among your heirs.

What is “Per Stirpes”?

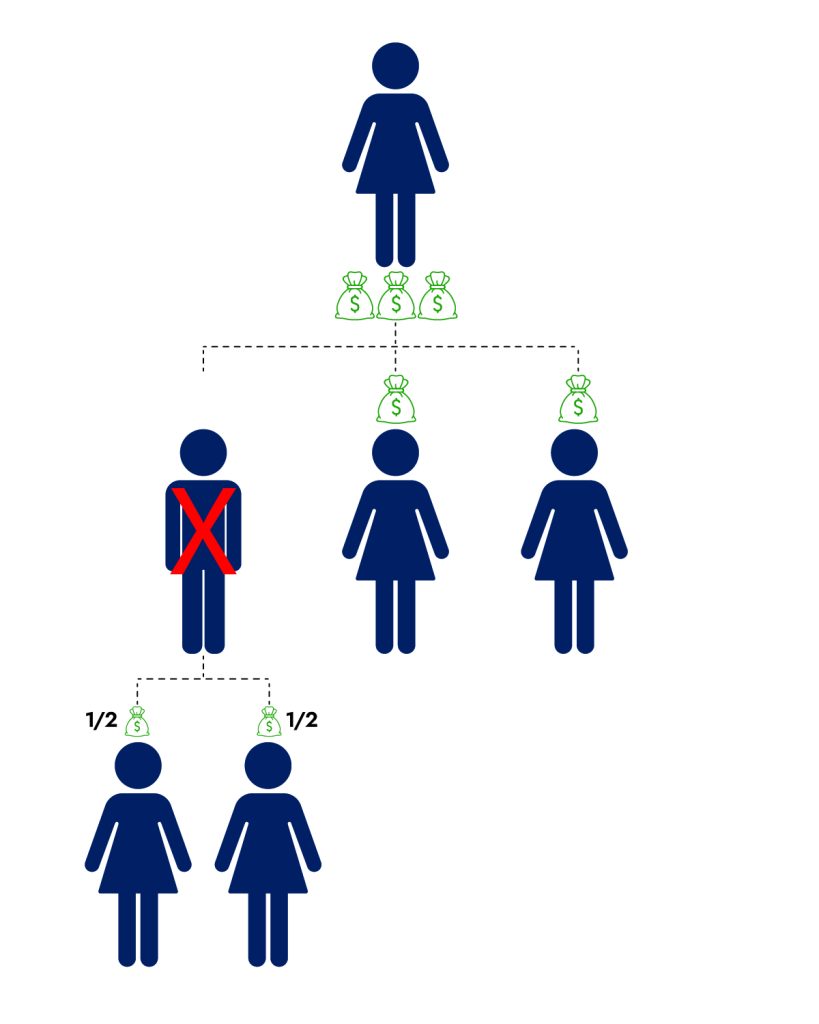

The term per stirpes translates to “by branch” and refers to dividing an estate among the branches of a family. This method ensures that if an heir predeceases you, their share will be passed on to their descendants. In other words, per stirpes keeps the inheritance within a specific family line.

Example: If you have three children, but one of them passes away before you, the deceased child’s share would be divided equally among their children (your grandchildren). The remaining two children would each receive their full share, and the deceased child’s share would be inherited by their descendants.

What is “Per Capita”?

Per capita, on the other hand, translates to “by head.” This distribution method divides the estate equally among all living heirs, regardless of their family branch. If one of your heirs passes away before you, their share does not get passed on to their descendants. Instead, the estate is divided equally among the remaining living heirs.

Example: If you have four children, but one predeceases you, the remaining three children would share the full estate equally. The children of the deceased heir would not receive anything, as the division happens equally among the surviving heirs.

While the difference between these two options may seem subtle, the impact on your loved ones can be significant. Choosing the wrong option—or failing to clarify your preference—could lead to unintended consequences, disputes among heirs, or even legal challenges.

Why Review Your Beneficiary Designations Now?

Life rarely stands still. Over time, your family dynamic and financial situation can shift. Perhaps you’ve welcomed new children or grandchildren, experienced a marriage or divorce, or lost a loved one. Each of these changes could alter how you want your assets to be distributed.

Outdated or incorrect beneficiary designations can result in assets being distributed contrary to your intentions. For example:

• A former spouse could unintentionally remain the beneficiary of a retirement account. If there is a per stirpes designation, any new children of the ex-spouse could stand to inherit a portion of the assets, in addition to your own.

• A child or grandchild born after you last updated your beneficiary designations could be left out entirely when using a per capita designation.

Without a clear understanding of per capita versus per stirpes, your heirs may not receive the inheritance you intended for them.

Which Method Should You Choose?

Choosing between per stirpes and per capita depends on your family dynamics and the goals you have for your estate. Here are a few considerations:

Per Stirpes: This method is often ideal for families with multiple generations or if you want to ensure that your descendants (grandchildren, for example) are taken care of. If your family includes children and grandchildren, per stirpes guarantees that each branch of your family is represented.

Per Capita: This method works best for families where you want an equal division of assets among the surviving heirs. It’s particularly useful if you prefer to ensure that all living heirs receive an equal share, regardless of how many generations are involved or descendants of a particular family line there are.

How Confluence Financial Partners Can Help

Your Wealth Manager can help you gather all your account and policy documents, check the names of the beneficiaries listed, the percentages assigned to each, and whether the designation is per capita or per stirpes. Furthermore, we can prepare a report summarizing the disposition of your estate to make sure it aligns with your wishes.

Ready to Make Changes?

Estate planning is complex, and small details can make a big difference. You may need to consult with your existing attorney to update your plan or your wealth manager can make an introduction to a qualified professional to draft a new one. Our team is here to help you navigate these decisions and help ensure your legacy is preserved. Call us today to schedule a personalized beneficiary review. Let’s work together to help ensure your estate plan reflects your current wishes and protects your family’s future. Don’t leave it to chance—act now to avoid unintended surprises tomorrow. Your peace of mind is worth it, and your loved ones will thank you.

Month in Review

Heading into 2025

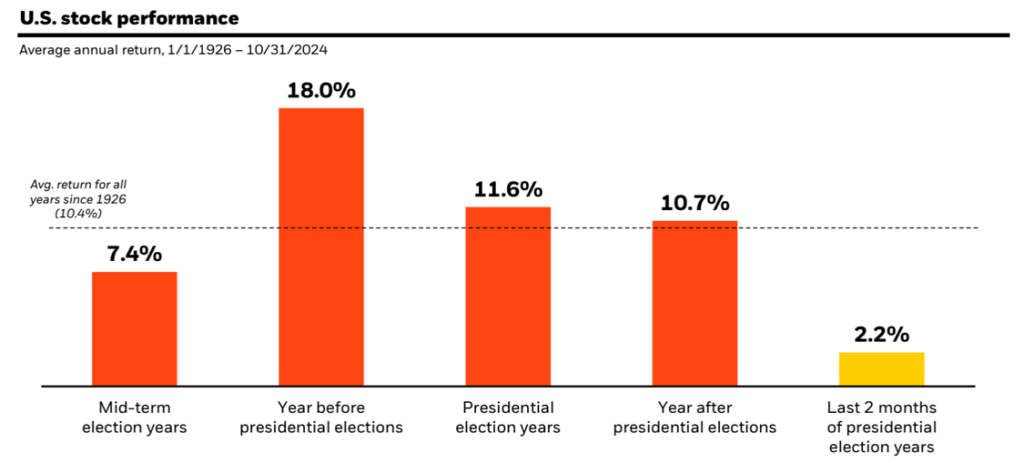

This year has been another strong year for equity markets, particularly US large-cap stocks. For example, the S&P 500 has made over 50 all-time highs in 2024, which is on pace for the fifth most in a calendar year since 1957. Through the end of November, it was also the strongest election year since 1936 for the S&P 500. What do investors have to look to as we head into 2025?

In the very near-term, investors have the month of December. Going back to 1928, the S&P 500 has had a positive return 74% of all Decembers, the highest positive return rate of any month. The average monthly return of +1.3% in December is the second-best month of the calendar year, on average.

There are also historical trends around US election cycles to consider. Since 1926, the S&P 500 has averaged +10.7% during the year after Presidential elections, slightly higher than the +10.4% for any given year. This trend largely reflects the ability for new administrations to enact legislative change prior to mid-term election years, which have historically had below-average results.

What’s on Deck for December?