Articles

Stock Market Recap: November 2024

Month in Review

Heading into 2025

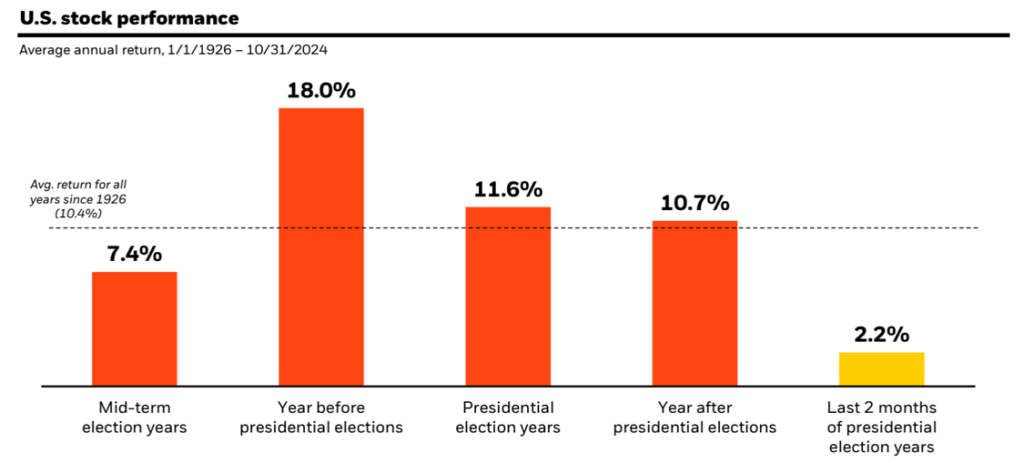

This year has been another strong year for equity markets, particularly US large-cap stocks. For example, the S&P 500 has made over 50 all-time highs in 2024, which is on pace for the fifth most in a calendar year since 1957. Through the end of November, it was also the strongest election year since 1936 for the S&P 500. What do investors have to look to as we head into 2025?

In the very near-term, investors have the month of December. Going back to 1928, the S&P 500 has had a positive return 74% of all Decembers, the highest positive return rate of any month. The average monthly return of +1.3% in December is the second-best month of the calendar year, on average.

There are also historical trends around US election cycles to consider. Since 1926, the S&P 500 has averaged +10.7% during the year after Presidential elections, slightly higher than the +10.4% for any given year. This trend largely reflects the ability for new administrations to enact legislative change prior to mid-term election years, which have historically had below-average results.

What’s on Deck for December?

Many companies offer equity compensation programs to attract, motivate, and retain top talent while conserving cash and aligning the interests of the employees and shareholders. While these incentive programs provide a great benefit, they must be carefully managed to avoid upsetting your financial strategy or posing a significant tax burden. Below we discuss two of the most common stock option plans that we help our clients understand and maximize.

As an employee, you may receive a Restricted Stock Unit (RSU) grant as part of your annual performance assessment or generally as part of your overall compensation package. The majority of RSUs have a vesting schedule, so you don’t receive the full value from the outset (Your employer wants to schedule vesting over a period, rather than all at once, to retain your services!). For example, if your company grants you 400 RSUs, you’ll probably get 100 shares to vest each year (typically on a quarterly schedule) until you vest all 400 shares, at which time you may receive a new grant.

RSUs give you an interest in the company but no actual value until they are vested. Upon vesting, the Fair Market Value (FMV) of the shares is considered income. You will then have the right to sell the vested shares and receive the cash proceeds or hold the shares for a longer period.

Regarding Taxes

Your income will include the FMV of the shares as they vest. You can sell your vested shares and convert them to cash. Alternatively, you may keep the shares, but any gains made after the vesting date would be taxed as capital gains when you sell. If you hold shares and they drop in value, you might be faced with selling those shares at a loss, while paying tax on vesting date FMV you never actually received.

Your employer typically handles your tax withholding at the vesting date by selling enough shares on your behalf to cover the estimated tax liability and distributing the remainder to you. The IRS requires a statutory 22% withholding rate. Because your vested RSUs influence your taxable income, and effective tax bracket, your employer’s tax withholding rate may not be enough.

Strategy

RSUs accrue over time and, if held, can lead to a significantly consolidated position in one firm. An experienced executive might start with 100 shares vested, then 200, then 300, and so on. Suddenly, they discover that a sizable chunk of their holdings, perhaps also a significant percentage of their net worth, consists of company stock.

Accumulation of company stock can lead to more than just lack of portfolio diversification. Generally, having a sizable stock position in the same company that also pays your salary isn’t advisable. If that organization, for a myriad of reasons, experiences a downturn this could have a double-whammy effect.

As a result, it may be advisable to sell all RSUs as they vest. There should be no additional taxes owed, because your costs basis will be the FMV at which you received the stock. In fact, keeping RSUs as they vest is the exact same thing as taking each cash bonus and investing it 100% in your company stock. If you wouldn’t do that, you shouldn’t hold all of your RSUs. By converting the shares to cash you will be better able to manage taxes due and invest proceeds in a more diverse manner. This should provide you with greater and more predictable long-term success.

Incentive Stock Options (ISO) are issued by public companies or private companies planning to go public in the future. They are most typically offered to executives and highly valued employees and are designed to encourage these employees to stay with the company over the long term.

An ISO provides an ‘option’ to purchase shares in a company at a set price, called the ‘strike price’, for a specified period. Like RSUs, ISOs are typically subject to a vesting schedule that could be several years. As the ISOs vest, you can exercise them at the strike price stated in the grant. Employees may have 10 years to exercise their options before they expire. Once you exercise vested shares, you now own the shares at the strike price. You may hold them or sell them immediately, but there are several things to consider.

Regarding Taxes

When you exercise your ISOs, you don’t receive any proceeds, as the exercise is only the purchase of the stock. To qualify for the most favorable tax strategy, ISOs need to be held for 2 years from grant date and 1 year after exercise, allowing for Long Term Capital Gains (LTCG) treatment at sale. Pursuing this strategy, however, can trigger what is known as Alternative Minimum Tax, or AMT.

This tax liability is created by the spread, or difference between, the Fair Market Value (FMV) and the Strike price you were granted. This is often referred to as the ‘Bargain Element’, and if large enough, will create AMT. This can be very complex and confusing as many employees are unaware of this and are caught off guard by their sometimes-significant tax liability due to AMT. We help our clients understand the AMT involved with their ISO strategy, and the ways that they can use any excess AMT payments as credits against future taxes in years where they aren’t subject to AMT.

Another option for ISOs is to do a “cashless exercise,” which means you never actually purchase the stock at the strike price, but rather you are simply paid out the spread between the strike price and the current FMV. This is a good choice if you don’t want to worry about AMT, or if you don’t have the cash necessary to buy the shares at the strike price. However, this strategy will cause the spread to be taxed at ordinary income rates instead of capital gains rates, and it effectively forgoes the potential tax benefits offered by ISOs.

Strategy

We generally recommend exercising options as soon as they vest and holding for long term capital gains treatment. Your specific strategy may vary based on your goals, but reducing what could be a concentrated position, and reinvesting the proceeds in a more diverse portfolio can lead to more predictable long-term outcomes.

The most common misconceptions about equity incentive programs relate to taxation and vesting.

If your employer offers these unique and valuable benefits, don’t let the financial planning overwhelm you. Act today and consult with an experienced financial planner and a tax professional to develop a solid strategy for maximizing your wealth. If we can help you in any way, please don’t hesitate to contact us.

March is National Nutrition Month!

This dedicated span of time encourages us to spotlight the significance of nutrition and healthy eating, recognizing this as a core pillar to both mental and physical well-being. I’m excited to dive into a topic that holds a special place in my heart – metabolic health. See below an introduction, as we explore how choices we make in dietary habits play a crucial role in shaping metabolic well-being – and what that even means!

The human body is intricately detailed and complex, similar to a car. While many of us don’t comprehend a car’s inner workings, we can sense when something is “off” and impacting optimal functionality. Similarly to a check engine light flipped on, there are many cues the body gives that it’s utilizing food for fuel less than optimally, such as the following: cravings, weight struggles, energy slumps, relentless fatigue, etc. Sadly, many of us have ignored these signals for too long.

The engine of the car is likened to the body’s metabolism. Just as the engine converts fuel into usable energy so the car can operate, being in good metabolic health ensures our body is able to generate and process energy efficiently to sustain life.

What factors determine metabolic health, you may wonder?

Clinically, it hinges on five specific and measurable factors¹:

According to the recent study published in the Journal of American College of Cardiology in July 2022, it’s estimated that only ~7% of adult Americans adults have optimal metabolic health, leaving 93% with markers in unhealthy ranges².

Each marker out of range increases the risk for development of complications like heart disease, Type 2 Diabetes, or stroke. Three or more out of range is considered metabolic syndrome. Getting an annual physical exam and bloodwork empowers your healthcare provider to evaluate your risk for metabolic syndrome. The good news is that lifestyle choices highly influence the health of these markers – namely eating a balanced diet and shunning a sedentary existence as two very practical realms to target.

Balanced Diet

Nutritionally, a balanced diet revolves around diverse, nutrient-rich whole foods while limiting processed items. A simple example of this would be choosing an apple (whole form) as opposed to apple sauce or apple juice, as often as is doable. This is due to the quality of nutrients the whole form contains as opposed to added processing.

When it comes to energy, the body’s preferred fuel source is glucose (think of this like gasoline), which comes from eating carbohydrates (carbs). In simplest terms, when we eat foods containing carbs, our blood sugars rise (as we expect). In those with good metabolic health, the body efficiently takes that glucose and converts it into usable energy and blood sugar levels are returned to normal through a process of hormonal “checks and balances”.

Conversely, poor metabolic health impedes glucose being used for energy efficiently, but rather leaves it in the blood stream, hence the term “high blood sugar”. When levels are high in the moment, you may experience the check engine symptoms listed above. Over time, chronically elevated blood sugar levels can lead to conditions like Type 2 Diabetes. When it comes to managing blood sugar levels – a quick tip you can implement today is the principle of “no naked carbs”.

No Naked Carbs

Clothing your carbs so they’re not “naked” means simply to pair a carb food with a protein or fat source to promote a steadier blood sugar response and limit a “spike” which may result from eating a carb only. Some examples would be peanut butter with a banana, cheese with crackers, or a hard boiled egg with grapes. This is just one simple tip to promote keeping your “engine” in tip-top shape, which will keep your body operating more efficiently in the moment and the long haul.

Sedentary Lifestyle

A sedentary lifestyle can be described as one marked by excessive sitting, lying down, and not engaging intentionally in physical activities that would increase heart rate or test muscle tone. For many Americans, especially depending on time of year and where one lives, this can include commute time to work, working from home sitting in front of a computer for most of the day, television watching, video game playing, etc.

Lack of movement, especially after eating food, can be disadvantageous for metabolic health as it can promote an “insulin resistant” state. Movement, like exercise (as simple as walking at a brisk pace or weight lifting) can promote “insulin sensitivity” which allows the body to utilize the incoming sources of foods more efficiently. The U.S. Department of Health and Human Services recommends the American adult to engage in physical activity categorized as moderate-intensity of 150 minutes per week and optimally 2 days of muscle strengthening, also³. This helps not only with metabolic health, but weight maintenance, mood, increasing “helpful” cholesterol (HDL), increasing creativity and promoting longevity, among many other benefits.

No matter where your starting point is, it’s time to get moving!

Let’s get your engine in check!

This introductory overview offers a flyover look into the intricacies of metabolic health, distinguishing between manifestations and potential risks. I hope you are encouraged that lifestyle factors like what you eat (good nutrition) and how much you move (exercise) can greatly reduce your risk for chronic disease, keeping your “engine” operating efficiently. By fostering awareness of the importance of metabolic health, we can be proactive in our approach to reducing risk factors. Time to take a look “under the hood” of your car!

Sources:

Healthcare Disclaimer: The contents of this article are meant for educational purposes and not to be misconstrued as medical treatment advice. Please speak with a qualified healthcare provider regarding personalized guidance regarding your specific medical condition before making changes to your unique plan of care.

Month in Review

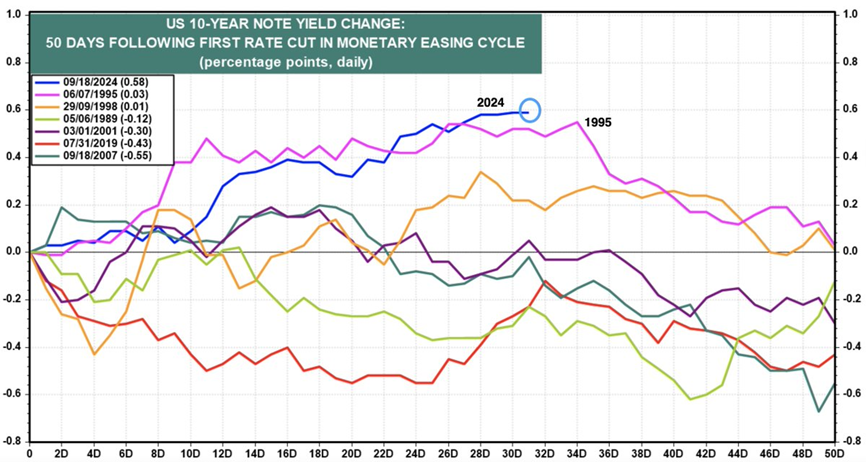

Why are Bond Yields Rising After the Fed Rate Cut?

The Federal Reserve began its interest rate cutting cycle in September, reducing the Federal Funds target rate by 0.50%. Historically, the start of an interest rate reduction policy has been associated with a decline in bond yields. Why is this? Typically, the Federal Reserve reduces interest rates to help support a slowing economy, whether its slowing due to changes in the business cycle, or an external event.

This year has been an exception, compared to the seven easing cycles since 1989 (before 1989 Federal Reserve did not officially target interest rate changes). Since the September 18th rate cut, the 10-year Treasury yield has increased nearly 0.60%, the largest increase at this stage compared to the previous seven cycles. It is worth noting that 50-days after the first rate cut, during the previous seven cycles, the 10-year yield was either the same, or lower, than the start.

What could be driving bond yields higher during the present cycle? It is likely the fact that inflation is declining, while the economy and jobs markets are still growing (at a slowing rate), similar to the 1995 soft landing outcome. Alternatively, it could be a sign that investors are concerned about the lack of any clear plan to address the US government’s fiscal situation. Measuring outstanding debt relative to annual economic growth, the United States has a debt-to-GDP ratio of 123%- meaning more debt outstanding than the rate of economic growth in a given year.

What’s on Deck for November?

If you’ve watched the news or browsed the web at all recently, no doubt you have seen the term “Bear Market” quite frequently. This term is often used when the worlds’ stock markets go through difficult periods, but what does it mean? And what should investors do about it? Here are five points to consider that will hopefully offer you perspective and confidence:

Key Takeaway: As difficult and unsettling as bear markets can be, it is important to understand that we “earn” the bull markets by being disciplined and patient during the bear markets. The reason that equities can make relatively high returns over time is that those returns are unpredictable in the short-term.

Sources: Capital Group, RIMES, Standard & Poor’s, 2020; MFS Market Insights, 2020; Vanguard Understanding market downturns, 2020; JP Morgan Guide to Markets, 2020.

Retirement plans can be confusing – we know! The decision of whether to contribute to a Traditional 401(k) or a Roth 401(k) is one that many people have or will encounter at some point in their lives. Although these two types of retirement accounts are very similar, they also have key differences. As more and more employers begin to offer a Roth 401(k) option, you should make sure that you have an understanding of each so that you can make the most informed decision possible.

The main difference between a Traditional or Pre-Tax 401(k) and a Roth 401(k) is the tax impact. With a Traditional 401(k), you receive a tax benefit for your contribution now, but are taxed on the withdrawals later. A Roth 401(k), however, does not provide a tax benefit now. As a result of paying tax on your contribution now, the Roth option allows for tax-free withdrawals later.

Here is a quick example to help explain the tax difference between the two options. This year, if you contribute $10,000 to a Traditional 401(k) and were taxed at a fictional rate of 15% (this would depend on your tax bracket) the $10,000 contribution would decrease your current year taxes by $1,500. If you contributed $10,000 to a Roth 401(k) instead, there would be no reduction to your current year taxes. If we fast forward to retirement and assume the $10,000 contribution is now worth $50,000, there will again be a difference between the two upon withdrawal. If you made a withdrawal of the entire $50,000, the full $50,000 would be taxed at your retirement tax rate with a Traditional 401(k), but the entire $50,000 would be withdrawn tax-free if it were originally invested in a Roth 401(k).

As you can see, the current tax benefit is greater with the Traditional 401(k), but the future tax benefits are better upon withdrawal from a Roth 401(k). One other item to note is that these facts hold no matter what the withdrawal amount is. No matter the amount, a withdrawal from a Traditional 401(k) is generally all taxable and a withdrawal from a Roth 401(k) is generally tax-free.

Unfortunately, the answer is that it depends. The primary question to ask yourself is: will my tax rate now or during retirement be higher? If you are in the beginning of your career or expect your income during retirement to be more than it is today, a Roth 401(k) may be right for you. If you believe your tax rate now is going to be higher than what it will be during retirement, then a Traditional 401(k) may be the best option for you.

Another advantage of the Roth 401(k) is that in addition to your original contribution, the growth of the account can be withdrawn tax-free! This is not the case with a Traditional 401(k). Also, if your employer provides a contribution match, you would need to pay tax on this portion of your account at the time of withdrawal whether you use a Traditional or Roth 401(k) as it is a pre-tax contribution.

There are several other differences between the Traditional and Roth 401(k) options that you may want to consider.

In summary, there is no easy answer to what type of 401(k) option is better. The decision will depend on your individual circumstances and most likely will change throughout your life. Using the information above should hopefully give you a good starting point to be able to make the most informed decision possible.

Please don’t hesitate to reach out to us if you would like to discuss further!

401(k) plans are long-term retirement savings vehicles. Withdrawal of pre-tax contributions and/or earnings will be subject to ordinary income tax and, if taken prior to age 59 1/2, may be subject to a 10% federal tax penalty. Roth 401(k) plans are long-term retirement savings vehicles. Contributions to a Roth 401(k) are never tax deductible, but if certain conditions are met, distributions will be completely income tax free. Unlike Roth IRAs, Roth 401(k) participants are subject to required minimum distributions at age 72. RMD’s are generally subject to federal income tax and may be subject to state taxes. Consult your tax advisor to assess your situation.

Any opinions are those of Gregory Weimer and Chuck Ziants and not necessarily those of Raymond James. This material is being provided for information purposes only and is not a complete description, nor is it a recommendation. Expressions of opinion are as of this date and are subject to change without notice. You should discuss any tax or legal matters with the appropriate professional.

Most parents appreciate the importance of traditional education in their child’s development considering the obvious intellectual and social benefits. Yet all too many forget that a financial education is also crucial for ensuring their offspring’s long-term well-being.The good news is it’s never too early or too late to begin sharing your financial wisdom and experiences with your family. By taking the time to teach your children the value of money, you’ll have the comfort of knowing they’ll understand how to care for their own financial legacy when the time comes.

Like reading, financial literacy is an essential skill, but unfortunately, it’s not typically taught in school. Rather, it’s up to parents to pass on their financial knowledge to ensure the next generation is capable of taking care of the wealth they’ve built.

Pre-kindergarten age is a great time to introduce the basics, including the idea that you must work to earn money in order to pay for items and services, as well as the value of different coins and bills. As they get a little older, your child can start doing chores and earning an allowance. Help them go through the motions of saving up for something they’d like to buy and deciding whether or not it’s a worthwhile purchase.

With pre-teens and teenagers, there are several other steps you can take, such as helping them open a savings account with their earnings from chores, babysitting or other jobs. Share your own tips on managing a budget and introduce them to the concept of investing and saving for retirement. Simply being transparent with your children about the realities and costs of living can go a long way in preparing them for the future.

While products such as trusts and wills can help ensure your wishes are carried out, they can’t give your heirs the true understanding of how to save, grow and spend money wisely. In fact, if your children are going to receive a sizable inheritance, they may get overwhelmed by sudden wealth without a solid foundation to rely on. It’s also a good idea to introduce your children, when they’re ready, to your financial advisor and other professional partners, so they’ll know where to find expert guidance when dealing with money issues.

Family and Life Events

August 14, 2019

Make Lasting Memories by Savoring Life’s Simple Joys

While extravagant vacations are great, you don’t need to spend a lot of money to make meaningful memories with your loved ones. A slow morning on the first day of summer. Baking cookies with the littles. A great meal surrounded by close friends or family. The best memories come in all shapes and sizes, both planned and unplanned. And while there’s nothing like going on that vacation you’ve been looking forward to for months, sometimes it’s the small, unexpected delights that stay with us the longest.

So how can you lead a life with more moments worth savoring? Here are a few tips to help you get started.

There’s nothing wrong with a bucket list full of exotic travel destinations or goals to buy that yacht or plan a big family reunion. After all, helping you work toward those goals is what a well-planned life is all about. Still, that’s usually not our day-to-day life. There are so many moments in between those grander experiences that are opportunities to explore smaller joys that, when added together, can be just as memorable or fulfilling as a big trip.

Start by picturing your perfect day. What do you do or eat? Who and what do you see? Perhaps it’s reading a book, listening to music or getting outside. Maybe you want to spend more time with close friends. After thinking it over, consider how to bring a few of those elements into your regular routine.

For example, maybe you want to get outside and see one of your friends more often. Consider putting a weekly date on the calendar with them to go for a walk, helping you fulfill both goals. Or perhaps you want to spend more time with your grandkids and also do more at-home cooking. Can the kids help? It could turn into an opportunity to not only spend time together, but for you to share some of your skills and insights with the next generation – doing something as simple as making a pizza.

When trying to find ways to bring the whole family together, consider what everyone is most interested in. Do your kids or grandkids have favorite activities you can do together? Maybe it’s going to an escape room or planning a watch party for their favorite show. Better yet, take turns choosing the plans for a monthly get-together. Experiences are a great way to connect and they make excellent gifts, too.

Social media has given us unprecedented access to loved ones near and far, and it’s made it easier than ever to share our lives (for better or for worse). But while it makes capturing a moment so easy, social media can also put extra pressure on ourselves and our experiences to be and look perfect – making it that much harder to cultivate and cherish authentic memories.

Moreover, according to Psychology Today, the average American has five social media accounts and spends an hour and 20 minutes each day browsing their feeds. That’s more than 37 hours every month! Imagine the memories we could create over a year with that time.

If you’ve found yourself getting sucked into social media, consider taking a break or limiting the time you spend scrolling. Time management apps and new settings on phones allow you to set timers so you receive an alert when you’ve gone over your allotted time on specific apps.

It’s hard to fully take in a great moment when we’re distracted, whether by our never-ending to-do list or our phone. Learning how to quiet our mind for even short periods of time can leave us open for moments of serendipity and spontaneity. Perhaps you run into a friend at the grocery store and decide to catch up over lunch, or spot a bed of flowers in full bloom while on a walk – both things you may have missed while checking your phone or worrying over all the errands on your list.

Meditation has been proven to help reduce stress and anxiety while improving our concentration. And with several popular apps out there with guided meditations, it’s never been easier to give it a try. While some require subscriptions, most offer a free trial so you can see how you like it before making a commitment.

Living for the moment is all about applying that stop-and-smell-the-roses mindset to your daily life. That way, even when you aren’t cruising the Mediterranean or celebrating your birthday with a bash, you might just stumble upon a few more exciting moments and soak up some extra memories along the way.

Sources: Psychology Today; Huffington Post

Raymond James is not affiliated with any organizations mentioned.

Family and Life Events

June 26, 2019

Check This List – Twice – Before Year-End

While keeping in mind your long-term investment goals, meet with your advisor and coordinate with your tax professional to examine nuances and changes that could impact your typical year-end planning.

Be thoughtful about required minimum distributions (RMDs) to ensure that you comply with the rules. If applicable and you have yet to do so, take your 2017 RMD to avoid a 50% penalty on required amounts not taken. Other considerations:

Evaluate whether you could benefit from tax-loss harvesting – selling a losing investment to offset gains or establish a deduction of up to $3,000. Excess losses also can be carried forward to future years. With your advisor, examine the following subtleties when aiming to decrease your tax bill:

Those at or near the next tax bracket should pay close attention to anything that might bump them up and plan to reduce taxable income before the end of the year.

From welcoming a new family member to moving to a new state, any number of life changes may have impacted your circumstances over the past year. Bring your financial advisor up to speed on major life changes and ask how they could affect your year-end planning.

Consider these to-dos as you prepare to make the most of year-end financial moves, and discuss with your financial advisor and tax professional:

*Withdrawals prior to age 59 1/2 may also be subject to a 10% federal penalty tax. RMDs are generally subject to federal income tax and may be subject to state taxes. Consult your tax advisor to assess your situation. Raymond James advisors do not provide tax advice.

TAX PLANNING

November 21, 2018

Redefining Your Retirement

Although an estimated 10,000 baby boomers reach retirement age every day, how each chooses to spend their free time can be quite different. Today’s retirees wish to forge new identities and seek new experiences, while redefining how they spend their time and money.

See if one or more of these new retiree profiles resonates with you. Deciding how you’ll stay busy can go a long way toward helping you plan and save for your dream retirement.

Givers contribute time, talent and, yes, even money to support causes close to their hearts. While the typical American spends 20 minutes a day engaged in volunteer, civic or religious activities, the Giver over age 65 dedicates a half hour or more, according to the Bureau of Labor Statistics.

One retiree may use her musical talents to play the violin for hospital patients, while another works behind the scenes updating a nonprofit’s website. Either way, it’s all about making a meaningful difference.

Note: Givers may become too altruistic, spending more time and money than planned, undermining health or financial stability.

Thinkers have a deep desire for lifelong learning. They may retire in a college town, take classes, read for pleasure and engage in contemplative activities.

Many colleges and universities are designing courses aimed at this new senior class. Campuses can be found in areas with affordable housing, quality education, teaching opportunities, walking and biking trails, and excellent transportation, healthcare and entertainment options.

Note: If you’ve established a 529 plan for a child or grandchild, you may be able to use unneeded funds for your own continuing education. Ask your financial advisor about potentially withdrawing funds without penalties.

Entrepreneurs typically start a business that’s different from a past career, bringing decades of experience, success, passion and emotional intelligence to their new ventures.

Goals include a fulfilling career, increased flexibility and enjoyment in their work. Some hope their new endeavors will becomes self-sustaining, while allowing for work/life balance.

Note: A small business entails a business plan, startup costs, insurance and a financial plan. Work with a professional tax planner and financial advisor to build a successful venture.

The Explorer dedicates up to a quarter of their financial resources on travel. These globetrotters invest in experiences and indulge their wanderlust while they have the health, energy and resources.

Good saving habits help Explorers immerse themselves among other cultures, foods and languages.

Note: Plan for ongoing travel expenses, desired location, frequency and duration, as well as inflation and foreign exchange rates. Health-related issues may become a limitation in later years.

The Part-Timer, like the Entrepreneur, seeks a career change, but may not wish to commit to a full-time position. Some favor mini-retirements – periods of work followed by intermissions for relaxation. Think consulting and contracting, for example.

Note: Returning to work, even part time, can incur expenses such as new work attire, transportation and dining out. Evaluate the impact of additional income on your current tax bracket, Social Security benefits, healthcare coverage, and potential contributions to retirement plans.

Foodies prefer quality dining and enjoying the experience of the meal. They typically spend about an hour and 20 minutes when dining, relishing how food and drink increases their quality of life. They enjoy experimenting with new creations, introducing new flavors or bringing friends and family together.

Since the Foodie spends time shopping for and preparing meals, other expenses are typically lower.

Note: Food connoisseurs need to factor in healthcare costs and inflation, as well as utilities and transportation.

The Athlete may compete in triathlons or play tennis into their 80s and beyond. They stay in top form and enjoy training and competition.

As the Athlete eventually slows down, or faces sudden illness or injury, healthcare costs can account for a significant share of retirement income, including Medicare expenses, prescriptions or long-term care needs.

Note: It’s important to budget for proper equipment and training. Select an appropriate Medicare or healthcare policy and account for expenses that aren’t covered. Be sure to factor in inflation and long-term care or assisted living.

Sources: Journal of Financial Planning: “How retirees spend their time”; Bureau of Labor Statistics; Robert S. Wilson, Ph.D., Rush Alzheimer’s Disease Center; Work in Retirement: Myths and Motivation; J.P. Morgan “Cost of Waiting” study; President’s Council on Fitness, Sports & Nutrition

Earnings in 529 plans are not subject to federal tax, and in most cases, state tax, so long as you use withdrawals for eligible education expenses, such as tuition and room and board. However, if you withdraw money from a 529 plan and do not use it on an eligible education expense, you generally will be subject to income tax and an additional 10% federal tax penalty on earnings. Investors should consider before investing, whether the investor’s or the designated beneficiary’s home state offers state tax or other benefits only available for investments in such state’s 529 savings plan. Such benefits include financial aid, scholarship funds, and protection from creditors. 529 plans offered outside their resident state may not provide the same tax benefits as those offered within their state.

RETIREMENT AND LONGEVITY

August 15, 2018